Social Finance Inc., the online lender that built a small empire reworking student debt, will announce a plan this week to refinance auto loans, the latest in a product push as it burnishes its own finances before an

expected public listing.The 10-year-old company is offering the service through a partnership with MotoRefi, a startup whose digital platform connects debtors with banks and credit unions and handles the tedious paperwork of reworking auto loans with state motor vehicle departments.

“We constantly hear from our members on what products they’d like us to offer, and auto loans have been a consistent request,” said Jennifer Nuckles, a SoFi executive vice president. “We also looked at our internal data and found that a large portion of our members carry large auto loan balances, and ... could benefit from refinancing.”

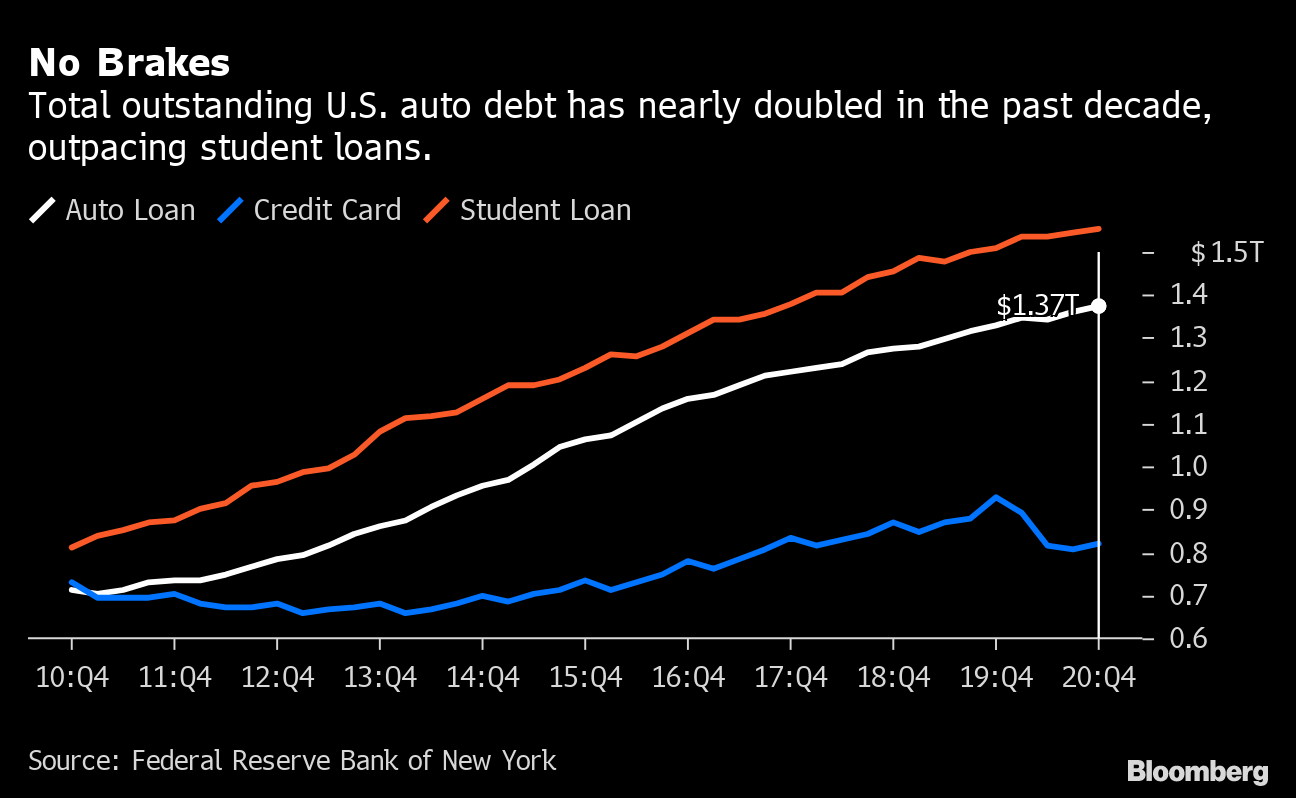

No Brakes

Total outstanding U.S. auto debt has nearly doubled in the past decade, outpacing student loans.

Source: Federal Reserve Bank of New York

MotoRefi essentially will embed its lending machinery in the SoFi site and will contribute a share of revenue for each transaction that comes through the new sales channel. Chief Executive Officer Kevin Bennett hopes SoFi’s scale and marketing clout, including its nearly 2 million customers at present, will drive awareness and expand the market. Only about $50 billion in U.S. auto debt is reworked in a given year, and only about half the people with a car or truck loan realize that refinancing is an option.

“It’s not a moment consumers think about, and we’re changing that,” Bennett said. “We think it’s absolutely reasonable to think that everyone who refinances their homes will refinance their car.”

MotoRefi launched in 2017 and handled $250 million in loans last year. It says its product is catching on quickly, because its customers can overhaul their debt via smartphone in just a few minutes. The company is aiming to process $1 billion in loans this year.

SoFi, meanwhile, is launching the service at a growing mountain of debt. As vehicle prices climbed in the past decade, U.S. consumers increasingly borrowed to buy new cars and trucks, in part because dealerships began offering longer loan terms, often up to seven years. Some 114 million Americans are collectively carrying $1.37 trillion in auto loans, according to the Federal Reserve Bank of New York; that’s 9% of all household debt. The number of car loans in the U.S. surged by 41% in the last decade as the total pile of debt nearly doubled, growing faster than any other category of borrowing, including student loans.

Down the Road

The number of U.S. auto loans surged by 41% in the past decade, far more than any other category of household debt.

Source: Federal Reserve Bank of New York

Financing has become a major profit source for car dealerships, many of which are able to leverage rates from captive, restless customers far higher than those available elsewhere. On average, MotoRefi says it is able to lower payments by about $100 a month. Although some of that reduction can come from consumers extending the duration of their debt, the company says its typical refinancing cuts an interest rate in half.

“The rates people get stuck with at the dealer is often unthinkable,” Bennet explained. “We refinance people who have 20 or 25% rates sometimes.” Still, borrowers have been slow to rework their vehicle loans, in part because many don’t realize that they can. Only about 4% of car loans are refinanced today, compared with about 20% of mortgages. For SoFi, the lack of awareness was a major incentive. “We looked across several offerings in the space,” Nuckles said, “and saw a massive, unmet opportunity.”

Auto refinancing is the latest in a series of new offerings for SoFi. In early January, the company agreed to merge with Social Capital Hedosophia Holdings Corp. V, a special purpose acquisition company founded by former Facebook executive Chamath Palihapitiya. The deal valued SoFi at around $8.7 billion. In the months since, the company has purchased a California bank, rolled out a new credit card and established a service to help customers invest early in IPOs.

https://ift.tt/3dCiqCD

Auto

Bagikan Berita Ini

0 Response to "Auto Loans Get Their SoFi Moment - Bloomberg"

Post a Comment